What Happens If You Miss Your Medicare Enrollment Period?

.

What Happens If You Miss Your Medicare Enrollment Period?

Enrolling in Medicare is an important step in protecting your health and financial well-being as you approach age 65. However, many people are unsure about the deadlines and enrollment periods, which can lead to missed opportunities to sign up for coverage. Missing your Medicare enrollment period can have several consequences, including delayed coverage and potential penalties. Understanding what happens if you miss the deadline can help you avoid unnecessary stress and costs.

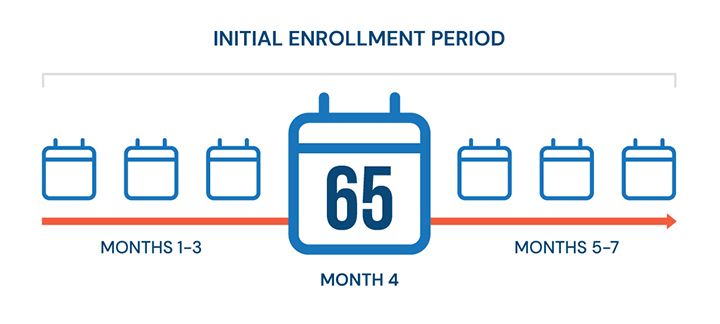

Understanding the Initial Enrollment Period

Your Initial Enrollment Period (IEP) is the first opportunity most people have to enroll in Medicare. This period lasts for seven months. It begins three months before the month you turn 65, includes your birthday month, and continues for three months after. An exception to this would be if your birthday is on the 1st of the month. In that case, you are eligible for Medicare the month BEFORE your 65th birthday.

During this time, you can enroll in Medicare Part A (hospital insurance) and Part B (medical insurance). Many people also explore options like Medicare Advantage plans, Medicare supplement plans or prescription drug coverage. Signing up during this window helps ensure your coverage begins on time and allows you to avoid late enrollment penalties.

Unfortunately, some individuals miss this window because they are unaware of the timeline, assume they are automatically enrolled, or simply forget to complete the enrollment process.

What Happens If You Miss Your Initial Enrollment Period?

If you miss your Initial Enrollment Period and do not qualify for another special enrollment opportunity, you may have to wait for the General Enrollment Period (GEP) to sign up.

The General Enrollment Period takes place every year from January 1 through March 31. If you enroll during this time, your Medicare coverage will typically begin July 1. This delay could leave you without coverage for several months, which could result in paying out-of-pocket for healthcare services during that time and cause penalties to accrue.

Potential Late Enrollment Penalties

One of the biggest concerns about missing your Medicare enrollment period is the possibility of late enrollment penalties.

For Medicare Part B, if you did not sign up when you were first eligible and you do not qualify for a Special Enrollment Period, you may have to pay a 10% increase in your monthly premium for every 12-month period you were eligible but did not enroll. This penalty is usually permanent, meaning you may pay the higher premium for as long as you have Medicare.

For Medicare Part D (prescription drug coverage), there may also be a late enrollment penalty if you go 63 days or longer without credible prescription drug coverage after your Initial Enrollment Period ends. This penalty is added to your monthly premium and may continue as long as you have a Medicare drug plan.

Special Enrollment Periods May Apply

In some cases, you may qualify for a Special Enrollment Period (SEP), which allows you to enroll in Medicare without penalties outside of the standard enrollment windows.

For example, many people continue working past age 65 and receive health insurance through their employer. If you have credible coverage through your employer or your spouse’s employer, you may be able to delay enrolling in Medicare Part B without a penalty.

When that employment or coverage ends, you typically receive an eight-month Special Enrollment Period to enroll in Medicare Part B. Acting quickly during this time is important to avoid gaps in coverage or late penalties.

There are certain requirements for your coverage to be considered credible to avoid penalties. Some of these center around the size of the employer carrying the group health plan and if the coverage is through active employment (not COBRA or retirement benefits).

How to Avoid Missing Your Enrollment Period

The best way to avoid missing your Medicare enrollment period is to plan ahead. As you approach age 65, it is helpful to start learning about your Medicare options and enrollment timelines. Mark important dates on your calendar and gather information about your current health coverage.

If you are still working or covered under an employer plan, verify whether that coverage is considered credible and understand how it may affect your Medicare enrollment.

Many people also find it helpful to speak with a licensed insurance agent or Medicare advisor who can explain the process and help them review their options.

The Importance of Getting Help

Medicare can feel confusing, especially if you are navigating the process for the first time. Missing an enrollment period can lead to delays and added costs, but understanding your options can help you move forward with the right coverage.

If you think you may have missed your Medicare enrollment period, it is important to seek guidance as soon as possible. An experienced Medicare professional can help determine whether you qualify for a Special Enrollment Period and explain the next steps for getting coverage.

Final Thoughts

Missing your Medicare enrollment period does not mean you are out of options, but it can create challenges such as delayed coverage and higher premiums. By understanding the enrollment periods and acting quickly when you become eligible, you can avoid many of these issues.

Taking the time to learn about Medicare and asking questions early can help ensure you have the coverage you need when you need it. If you are approaching age 65 or have questions about enrollment, reaching out for assistance can make the process much easier and give you peace of mind as you move into this next stage of healthcare coverage. Call our office today to learn more.